Скачать презентацию

Идет загрузка презентации. Пожалуйста, подождите

1

Фландрия: окно в Западную Европу

2

Flanders Investment & Trade Важный партнёр для иностранных компаний для выхода на европейский рынок, через Фландрию (Бельгия) Конфиденциальность услуг Индивидуальный подход

Конфиденциальность услуг Индивидуальный подход")

3

Преимущества Фландрии

4

Фландрия : окно в Западную Европу Преимущества Фландрии: Расположение в самом центре Европы Отличная транспортная инфраструктура Всемирно признанные высокопрофессиональные трудовые ресурсы Разнообразные налоговые льготы Высокотехнологические исследовательские центры Лучшие показатели в международных рейтингах и исследованиях Высокий уровень жизни для иностранных специалистов Значительная поддержка правительством Фландрии

5

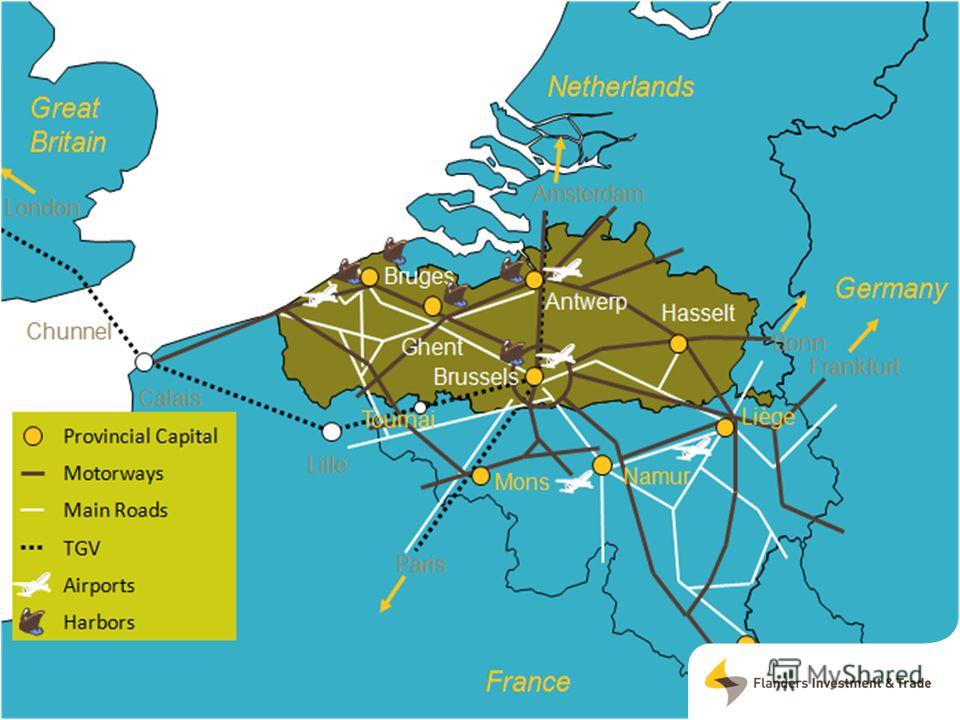

Стратегическое расположение Уникальное географическое pасположение на перекрёстке eвропейских дорог Самое сердце Европы с штаб-квартирой Европейского Союза, НАТО и т.д. Порт Антверпен

6

Бельгия - сердце Европы

7

Экономический двигатель Европы: "Золотой банан" Содержит 80% покупательской способности в ЕС

8

Брюссель Столица Фландрии Столица Бельгии Столица Европы Мультикультурный Многонациональный Многоязычный … где бьется сердце Европы!

9

Великолепная транспортная инфраструктура Отличная сеть дорог (бесплатные дороги) Значительная сеть железнодорожных и внутренне- водных дорог с выходом в наиболее важные рынки Европы 4 международных морских портов : Антверпен, Гент, Зи-Брюгге и Остенде Максимум 2 часа езды до международного аэропорта: один из крупнейших грузовых терминалов Европы

Значительная сеть железнодорожных и внутренне- водных дорог с выходом в наиболее важные рынки Европы 4 международных морских портов : Антверпен, Гент, Зи-Брюгге и Остенд")

11

Порт Антверпен Крупнейший порт в Европе для перевозки крупногабаритных грузов: N° 1 стали N° 1 фруктов N°1 лесной продукции 2-й крупнейший в мире нефтехимический кластер Возможности для инвестиций –Co-siting –Saeftinghedock: 1073 ГА

12

Порт Гент Крупнейший порт в мире по импорту фруктовых соков Крупнейший производственный и R&D кластер биотоплива в Европе Возможности для инвестиций: –Kluizendok: 660 ГА

13

Порт Зи-Брюгге Крупнейший хаб для новых автомобилей Крупнейший терминал для лесной продукции Европейский центр производства TROPICANA продуктов (часть европейского центра FOOD) LNG- терминал отвечает за более чем 15% от общеевропейских газораспределительных сетей

LNG- терминал отвечает за более чем 15% от общеевропейских газораспредели")

14

Порт Остенде Расположен в наиболее занятом морском регионе Универсальный морской порт с судоходными линиями на коротких расстояниях Быстрорастущий порт ро-ро Основные и насыпные: Ferro silicum, timber, fertilisers… Возможности для инвестиций: –Возобновляемые источники энергии и Offshore Ветроэнергетика

15

Bысокопрофессиональные трудовые ресурсы Многоязычная, высоко образованная и продуктивная рабочая сила Гибкость: Работа в выходные дни допускается В некоторых секторах допускается рабочий день до 10 часов Одна из самых упрощённых процедур получения разрешения на работу для иностранных офисных работников среди европейських стран

16

Фламандские университеты – лучшие в Европе Католический Университет Лёвен: –научно-исследовательский –международно-ориентированный Университет Гент: –плюралистический –ниши Университет Антверпен: –предпринимательский подход

17

Высокотехнологические исследовательские центры : High quality and availability of R&D RankingAvailability of latest technology Capacity for innovation Quality of scientific research institutions Availability of scientists and engineers Belgium Netherlands Germany France UK (The Global Competitiveness Report World Economic Forum 2012)

18

Уровень качества (Source: fDi Intelligence, from the Financial Times Ltd)

")

19

Высокий уровень жизни высокий стандарт жизни для иностранных специалистов превосходная система здравоохранения и образования, обеспечение всех условий для полноценной работы и жизни

20

ПОСЕТИТЕ НАШ ВЕБ-САЙТ! Thomas Castrel Заместитель Директора Департамент Внутренних Инвестиций Flanders Investment & Trade Tel: | Fax: Gaucheretstraat 90 | BE-1030 Brussels-Belgium

21

Invest in Belgium Tax aspects of doing Business in Belgium Marc De Mil – Federal Public Service Finance

22

Belgium Main Tax Incentives Corporation Notional Interest Deduction (NID) Numerous fiscal treaties to avoid double taxation Innovative measures to support R&D Patent income deduction Investment deduction for R&D related investments and patents Income tax reduction for researchers Ruling practice : legal certainty for investors Shareholder No taxation on capital gain Management Reduction of employment costs for expatriates, with simple proceedings

Numerous fiscal treaties to avoid double taxation Innovative measures to support R&D Patent income deduction Investment deduction for R&D related investments and patents Income")

23

Belgium Effective (Average) Corporate Tax Rate (ECTR) 2012* Sources : Taxation trends in the EU 2012 edition, Eurostat Tax Rates of OECD Countries, AEI International Tax Database, OECD Tax Database and World Bank *(based on asset and source of finance) Especially in Belgium, the ECTR is considerably below statutory tax rates (-8,1%) 23

Corporate Tax Rate (ECTR) 2012* Sources : Taxation trends in the EU 2012 edition, Eurostat Tax Rates of OECD Countries, AEI International Tax Database, OECD Tax Database and World Bank *(based on asset and source of financ")

24

Belgium Effective (Average) Corporate Tax Rate (ECTR) 2012* *(based on asset and source of finance) Especially in Belgium, the ECTR is considerably below statutory tax rates (-8,1%) Belgium Italy Germany Netherlands USA France UK Japan 24 Sources : Taxation trends in the EU 2012 edition, Eurostat Tax Rates of OECD Countries, AEI International Tax Database, OECD Tax Database and World Bank

Corporate Tax Rate (ECTR) 2012* *(based on asset and source of finance) Especially in Belgium, the ECTR is considerably below statutory tax rates (-8,1%) Belgium Italy Germany Netherlands USA France UK Japan 24 Sources : T")

25

What is it? A notional interest calculated and deducted yearly from the taxable basis Used to off-set operational or financial income (thus lowering effective tax rate) Notional Interest Deduction Who? Companies subjected to Corporate tax Non-residents / Corporate Tax

Notional Interest Deduction Who? Companies subjected to Corporate tax Non-residen")

26

How does it work ? Annual Tax Deduction = EQUITY X RATE Notional Interest Deduction

27

EXAMPLE 1: (Return on Equity: 4%) AssetsLiabilities Group Financing Share Capital P&L AccountBefore N.I.D.After N.I.D Profit before tax N.I.D. (3%)/ Taxable Corporate Tax (33,99 %) Effective Tax Rate 33,99 % 8,5% Notional Interest Deduction

AssetsLiabilities Group Financing 100.000 Share Capital 100.000 P&L AccountBefore N.I.D.After N.I.D Profit before tax 4.000 N.I.D. (3%)/- 3.000 Taxable 4.000 1.000 Corporate Tax (33,99 %) 1359340 Effective Tax Rate 3")

28

EXAMPLE 2: Net Result (Return on Equity) Effective Tax Rate 3 %0 % 4 % (Previous slide)8,5 % 5 %13,5 % 6 %17 % Notional Interest Deduction

Effective Tax Rate 3 %0 % 4 % (Previous slide)8,5 % 5 %13,5 % 6 %17 % Notional Interest Deduction")

29

Qualifying » equity ? Equity = total equity as defined under Belgian GAAP (includes retained earnings) in the opening balance sheet of the taxable period adjusted to avoid double use and abuse. Notional Interest Deduction Interest Rate ? Fixed yearly for 2012 (Tax Year 2013) : 3 % + 0,5 % 3,5 % (SME)

in the opening balance sheet of the taxable period adjusted to avoid double use and abuse. Notional Interest Deduction Interest Rate ? Fixed yearly")

30

Extensive tax treaty network

31

No WHT No LOB 10% shareholding 12 months Parent company – Ukrain (treaty partner) Belgian subsidiary Dividend withholding tax exemption

Belgian subsidiary Dividend withholding tax exemption")

32

People Wage withholding tax exemption Tax allowance for additional employee Innovation premium Expatriate tax regime Belgian R & D Centre Activities Investments Patents Favourable transfer pricing rulings Investment deduction R&D Tax credit Accelerated depreciation Tax exoneration for regional grants Deduction of gifts Patent Income Deduction Unique tax features for R & D

33

Patent Income Deduction What is it ? Deduction of 80% of the income from patents from the taxable basis, resulting in an effective tax rate of maximum 6.8% on this income. Who can benefit ? Belgian companies and Belgian establishments of foreign companies.

34

Patent Income Deduction Patents concerned. Applies to patents or supplementary protection certificates: self-developed by a Belgian company or branch in R&D centers (*) in Belgium or abroad; acquired by a Belgian company or branch provided they are being further developed in R&D centers (*) in Belgium or abroad; licensed to the Belgian company or branch provided they further develop in R&D centers (*) in Belgium or abroad. (*) R&D center must qualify as branch of activity.

in Belgium or abroad; acquired by a Belgian company or branch provided they are b")

35

Patent Income Deduction Calculation of the deduction. for patents that are licensed: 80% of the patent income received, to the extend the income is at arms length; for patents that are used in the production process: deemed deduction of 80% of the at arms length royalty that would have been received had the patents been licensed to unrelated third parties;

36

Investment deduction in R&D centres For assets which aim to promote R&D of new products and advanced technologies which are environment-friendly In one go: 15.5% of the investment value Spread deduction: 22.5% of the annual depreciation Investment deduction in patents In one go: 15.5% of the investment value No spread deduction Carry forward in case of insufficient profits, for an unlimited period. Investment deduction for investments in R&D centres and patents

37

Partial exemption salary withholding tax for researchers Principle: the withholding tax is normally retained on the remuneration paid to the researchers, but the employers are exempt from paying a part to the Belgian Treasury (more financial resources for the research activities) Researchers: Masters degree or equivalent Exemption: 75% of the withholding tax for all researchers

38

For foreign executives and managers temporarily detached in Belgium : Tax free expatriate allowance (cost of living, cost of housing, tax equalization) operational entity: / an HQ or R&D centre: / an Reimbursement of non-repetitive expenses (installation costs, moving expenses, school fees) unlimited amount tax free « Travel exclusion »: workdays performed outside Belgium: tax free in Belgium Expatriate status

operational entity: 11.250 / an HQ or R&D centre: 29.750 / an Reimbursement of non-repetitive expe")

39

For employers No tax, no social security contributions on expatriate allowances and reimbursement of expenses Deductible from corporate income Expatriate status

40

Characteristics of the Belgian ruling Ruling on all kind of taxes (Corporate, Personal, VAT,..) Case-by-case ruling in a new open culture Legal certainty for investors In accordance with international rules Open to potential AND existing investors Legally binding for a 5 year renewable period Economic substance required Tax Ruling

Case-by-case ruling in a new open culture Legal certainty for investors In accordance with international rules Open to potential AND existing investors Le")

41

Federal Public Service Finance Fiscal Department for Foreign Investments Rue de la Loi, 24 (Parliament Corner) 1000 Brussels - BELGIUM Marc DE MIL Tel.: Cell : Contact Federal Public Service Finance Fiscal Department for Foreign Investments Rue de la Loi, 24 (Parliament Corner) 1000 Brussels - BELGIUM Marc DE MIL Tel.: Cell :

1000 Brussels - BELGIUM Marc DE MIL Email: marc.e.demil@minfin.fed.bemarc.e.demil@minfin.fed.be Tel.: +32 257 870 19 Cell : +32 4707 870 19")

Еще похожие презентации в нашем архиве:

for Enhancing Ukraines Integration into.")

DCF valuation (e.g. using WACC) Relative valuation (comparables) Relative valuation.")

Finance Academy, Moscow E-mail: adamova karina@rbcmail.ru.")

October 2012.")

Proprietorship Partnership Corporation Co-operative.")

is broadcasting made, financed and controlled by the public, for the public. It.")

- a person whose profession is to provide qualified legal assistance.")